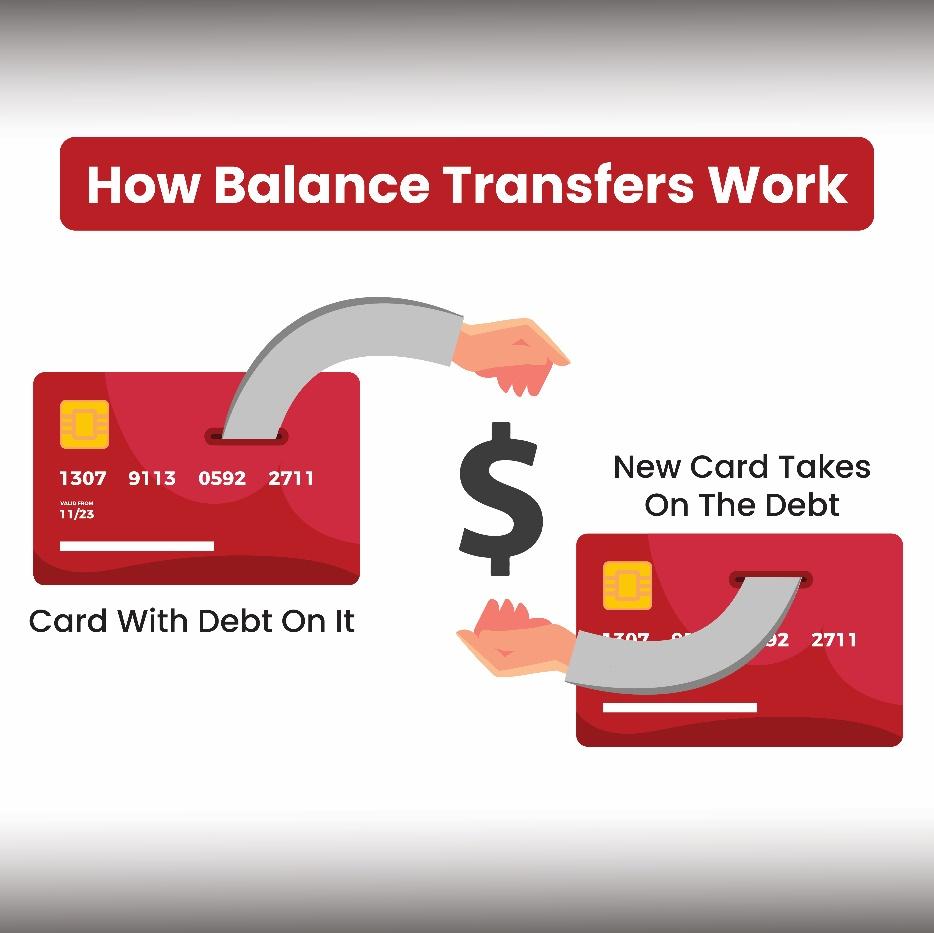

At first glance, a balance transfer credit card in Canada looks like a financial lifeline. Struggling with high-interest debt? A low or even 0% introductory rate sounds like the perfect solution. You move your existing balance to a new card, enjoy months of interest relief, and use that time to pay off your debt faster. Simple, right?

Not always.

What many Canadians don’t realize is that balance transfer credit cards come with fine print that can quickly turn a good deal into a financial setback. Hidden fees, skyrocketing interest rates after the promotional period, and risky spending habits can leave you worse off than before.

So, how do you take advantage of a balance transfer credit card in Canada without falling into the traps that cost you more in the long run? Let’s explore the mistakes to avoid, how to use balance transfers strategically, and some of the best options available today.

Mistake #1: Ignoring the Transfer Fee

Most balance transfer offers charge a balance transfer fee—a percentage of the amount you move to the new card. It typically ranges from 1% to 3%, but some can go higher. While this may seem small, on a $5,000 transfer, a 3% fee means you’re immediately paying $150.

The Scotia Value Visa is a great option for those looking to minimize costs, offering one of the lowest interest rates on balance transfers in Canada. If you’re considering a balance transfer credit card in Canada, this is one to check out.

Before you make a move, calculate whether the interest savings outweigh the transfer fee. If the fee is too high, the transfer may not be worth it.

Mistake #2: Not Paying Off the Balance Before the Introductory Rate Ends

Many balance transfer credit cards come with an ultra-low introductory interest rate—sometimes as low as 0%—for a set period, usually six to twelve months. However, once this period expires, the interest rate often jumps significantly, sometimes exceeding 20%.

This is where many people get caught. They transfer their balance, make minimum payments, and assume they’re in the clear. But when the promotional period ends, they’re suddenly stuck with high interest all over again.

The MBNA True Line Gold Mastercard offers a low ongoing interest rate, making it a great alternative if you need more time to pay down your balance. Instead of jumping to a high post-promotional rate, this card provides more manageable long-term repayment terms.

To avoid this mistake, create a repayment plan. Divide your balance by the number of months in the promotional period and commit to paying off that amount each month.

Mistake #3: Continuing to Use Credit Without a Repayment Plan

One of the biggest dangers of a balance transfer credit card in Canada is the temptation to continue spending. Many people transfer their existing balance but then continue to use their old credit card, racking up more debt. Now, instead of paying off their balance, they’re doubling it.

The key to using a balance transfer wisely is discipline. Once you transfer your balance, stop using the old credit card until your debt is paid off. If necessary, put it away or even cancel it to remove the temptation.

The Scotia Momentum No-Fee Visa offers a great alternative for everyday spending while keeping costs low. It provides cash back on everyday purchases, allowing you to earn rewards without carrying a balance.

Mistake #4: Overlooking the Standard Interest Rate on New Purchases

A common misconception is that the low balance transfer rate also applies to new purchases. In reality, most balance transfer credit cards charge a different, often much higher, interest rate on new spending.

For example, if your card has a 0% balance transfer rate but a 19.99% standard purchase interest rate, any new purchase will start accruing high interest right away. This is why it’s crucial to separate balance transfer cards from your everyday spending.

If you need a card for new purchases, consider the Scotia Momentum Visa, which offers cash back on spending while maintaining competitive interest rates.

Mistake #5: Choosing the Wrong Balance Transfer Credit Card

Not all balance transfer offers are the same. Some offer a lower interest rate but a shorter promotional period. Others charge higher transfer fees. Choosing the right card depends on your repayment strategy and financial situation.

Here’s a breakdown of some of the best balance transfer credit cards in Canada:

- Scotia Value Visa – A strong option with one of the lowest interest rates on balance transfers, making it ideal for long-term repayment.

- MBNA True Line Gold Mastercard – Offers a low standard interest rate, reducing the risk of high charges once the promotional period ends.

- Scotia Momentum No-Fee Visa – A no-annual-fee card that provides cash back on everyday purchases without adding financial burden.

- Scotia Momentum Visa – Ideal for those who want to combine balance transfers with everyday spending rewards.

How to Use a Balance Transfer Credit Card Wisely

A balance transfer credit card in Canada can be a powerful financial tool when used strategically. It allows you to consolidate existing credit card debt onto a new card, typically with a low or 0% introductory interest rate for a set period. This can significantly reduce the amount of interest you pay, giving you a chance to tackle your debt more efficiently. However, to make the most of a balance transfer credit card, it’s essential to understand how it works and use it responsibly.

First, take the time to fully understand the terms and conditions of the card you’re considering. Many balance transfer cards offer enticing promotional rates, but these low or 0% interest periods don’t last forever. Carefully review details such as transfer fees, the duration of the promotional period, and what the interest rate will be once the introductory offer expires. Some cards charge a balance transfer fee, which is typically a small percentage of the transferred amount, while others offer no-fee transfers as an added incentive. Knowing these details upfront will help you make an informed decision and avoid unexpected costs.

Once your balance has been transferred, it’s crucial to create a repayment plan to eliminate the debt before the promotional period ends. The goal should be to take full advantage of the low or 0% interest rate by paying off as much as possible—ideally, the entire balance—within the allotted time frame. Without a clear plan, you could find yourself back in a high-interest situation when the regular rate kicks in, often leading to more financial strain.

It’s also important to resist the temptation to make new purchases on your balance transfer card. Many people see a balance transfer as an opportunity to free up more spending power, but this can quickly lead to a cycle of accumulating new debt while still trying to pay off the transferred balance. Treat the balance transfer as a financial reset rather than an excuse to spend more.

Finally, choosing the right card is key to maximizing the benefits of a balance transfer. Consider factors such as the length of the promotional period, whether the card charges a transfer fee, and the ongoing interest rate after the promo period ends. Some cash back card options also offer balance transfer features, which can provide long-term value beyond just debt repayment. Selecting a card that aligns with your financial goals ensures that you not only get out of debt faster but also build better financial habits moving forward.

Final Thoughts

Balance transfers can be an excellent strategy for managing and reducing debt, but only if approached with a clear plan. The biggest mistakes come from misunderstanding the terms, failing to pay off the balance in time, and continuing to spend recklessly.

If you’re considering a balance transfer credit card in Canada, take the time to research and select the best option for your needs. Whether it’s the Scotia Value Visa for long-term low interest, the MBNA True Line Gold for a balanced approach, or the Scotia Momentum cards for cash back benefits, the right choice will depend on your financial habits.

By using balance transfers wisely, you can regain control of your finances and set yourself on a path to becoming debt-free.

Where to Apply?

If you plan to apply for a cash back rewards credit card, head to Great Canadian Rebates. Our online platform will allow you to compare the best cashback credit cards, which will help you choose the one that fits the bill. You can earn a solid credit card rebate when you sign up for the credit card through our platform.